Monzo Adds Overdraft Option

In August 2017, the British neo-bank Monzo first mentioned integrating overdrafts as an option made accessible via their iOS app, they called the service “Monzo Overdraft”. Tests have been run with some select customers, helping Monzo understand their expectations as regards to overdrafts and, mostly, make it transparent and easy for them to access this service. The challenge seems to have been met since this option is now proposed to all their customers.

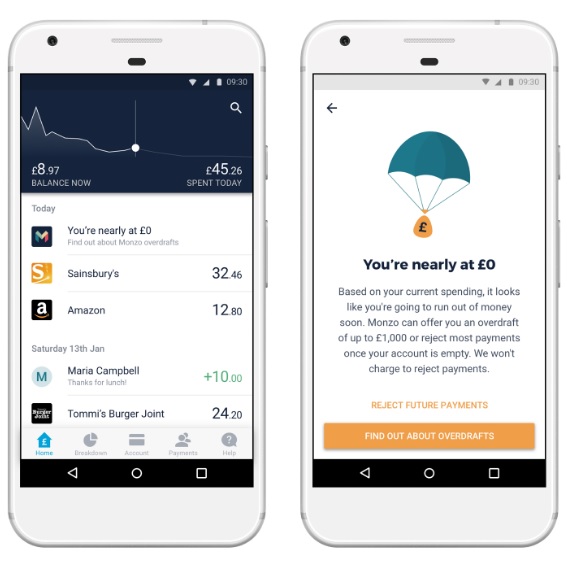

Monzo charges £0.50 per day in overdraft charge (maximum £15.50/month). They also plan that this overdraft fee should only apply a £20 buffer (people won’t be charged up to -£20). They are sent a notification to their mobile as soon as this limit comes close, and are informed when charged.

Payments that would cause the overdraft limit to be exceeded are rejected automatically, so customers can avoid bank intervention fees. Same applies when the customer’s balance reaches zero, if he did not choose the overdraft option.

Monzo explains that overdrafts are “totally optional”. Customers are invited to enable the feature themselves via their mobile app. In some cases, Monzo reserves the right to check their credit history –since this might affect the customer’s credit score.

Comments – Monzo makes overdrafts transparent for their customers

Monzo only provides some customers –meeting specific eligibility criteria– with the possibility to use this option. These criteria are also based on information from the credit rating agency, Callcredit. This FinTech calls on their customers’ own responsibility and insists on transparency, through making this information accessible via their mobile app. This notion of transparency is also highlighted by much guided customer processes (notifications, clearly stated limits, flat rates).

Monzo stresses a positive image as regards to a product considered stressful by most customers and often crystallises dissatisfaction since it involves banking fees. This product is in line with Monzo’s intent to make it easier for customers to manage their day-to-day expenses. Same goes for taking credit history into account since Monzo tries to be reassuring and to minimise potential impacts.

The neo-bank with 500,000 new customers for their current account (as announced last month) stands out as a British leader. They intend to stand out compared to traditional banking institutions.